When you are trying to gauge the effect of a news or fundamental item on a particular market you might be able to do so by determining the number of events which are "in the news" and being operated on by traders at that moment.

In the pits at the moment of an economic release of some magnitude the usual pit trader is strictly operating on the immediate news of the release. In the case of a financial future such as the S&P etc, this singularness of attention has a differing time span. As an index a futures mini contract is also impacted by individual stock news and buying/selling pressure and other factors shortly after the release regardless of what occured.

In order to get a momentum in a direction a singular story must dominate the market being traded. The more stories that are in play the more choppy the market is likely to become.

If a market normally has 20 different news items which could be seen to in some small way affect it, normally then it would have about that many when it was trading a normal variation in its price during a day.

If however it normally has twenty but only a single story exists for the day or a portion of the day as far as effect on the market, you are likely to see that security trade outside of its normal variation, and as a practical measure of this you could look at bollinger bands or extreme stochastics which repeat at those extreme levels.

This would be helpful in establishing exits for positions taken on news and for determining when the news has become diluted and is no longer a singular focus of trading. A bollinger setup or other indicator set up so as to show a divergence from the extreme reading would have you exiting such a position, if not initiating a new one for a reversal.

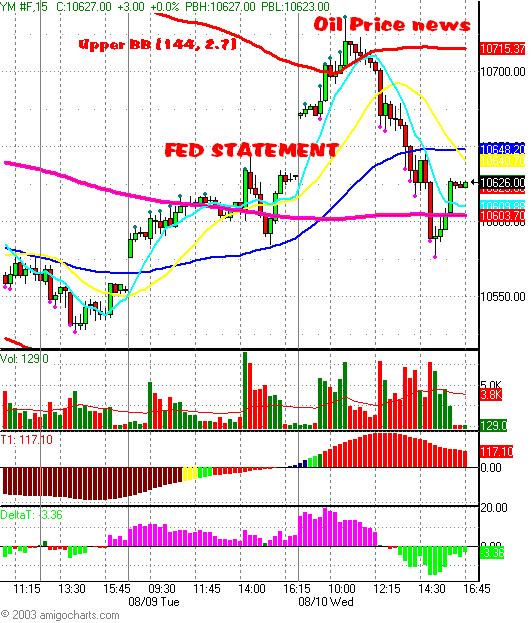

An example of this type of market action occured over the last two trading days: The first singular event was the fed releasing its outlook for the economy and it being a focus of trading in a positive way, moving the dow up considerably with a gap up that was further bought.

However, the momentum on this changed when oil prices, which had been static previously moved up dramatically. The market then sold off dramatically and the afternoon session focused a great deal on this.

So you had one big main singular story, which then ran its course, and was set aside for another one. What chop existed was simply the argument between the two stories as viewed by investors and traders. Other smaller stories existed, but did not affect the market in the same fashion and could be discounted to a marked degree.