In Futures trading it is a fact that for every dollar gained by one trader a dollar is lost by another. This is then further tipped to the losing side of the equation by the fact of expenses such as commissions, spreads, fees and costs associated with the trading(slippage).

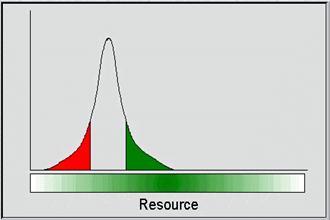

Since every contract is equal in value the volume at price is important from a standpoint of probability of trading success.

For example if 70 % of all contracts traded traded below a certain price then it could be viewed in a vaccum of any other data that it was likely that only 30% of those who bought at or above that price were able to profit from the position they took, and it could also be postulated that even less would actually make money after taking into account slippage.

Of course the price and distribution of percentages is always changing, so in order for this to have a workability volatility would need to be factored in on the same basis.

Example A: Buy YM at 10580, knowing that in the last several weeks the volume traded for YM under 10580 has been a mere .5% of the total volume. Taking into account the volatility while YM has been trading for that recent period you could arrive at an actual standard deviation of around 34. Taking into account the slippage you may encounter and commission and other trading costs you have figured you must trade with a 2 to 1 minimum risk reward ratio. You could then determine that any trade below 10563 (17 points) would then trigger a stop. Looking at it this way you could also set up your buy lower in a conservative manner to further cut down your risk.

Additionally you could on an ongoing basis monitor the immediate short term volatility of YM by using Bollinger bands which together create the characteristic that some bounce in a sell off results from their being touched and then moved away from. As with the total value of contracts, additionally this would factor in your favor - where the downside risk in a long position (or vice versa) would have proven to occur a low percentage of recent times.

Of course this is now developing into a trading strategy which is specific, but that is just an example. Any set of indicators which can be shown to occur with a bias that is substantial could be used to further increase the odds of a successful trade.

The point being here that the volume of trading distribution which is likely to affect your trade's expected duration should be taken into consideration and used to your advantage to determine a lower risk higher reward entry and exit.